By: Gulraiz Khalid

Africa is one of the most consequential frontiers in connectivity today. Mobile networks already power commerce, public services, and social inclusion at massive scale—and satellites are quickly becoming the connective tissue that extends those benefits into hard-to-reach places. The numbers make the case: in 2024, mobile technologies and services generated $220 billion of value—7.7% of Africa’s GDP—and the contribution is still rising.

The mobile base is large—and still expanding

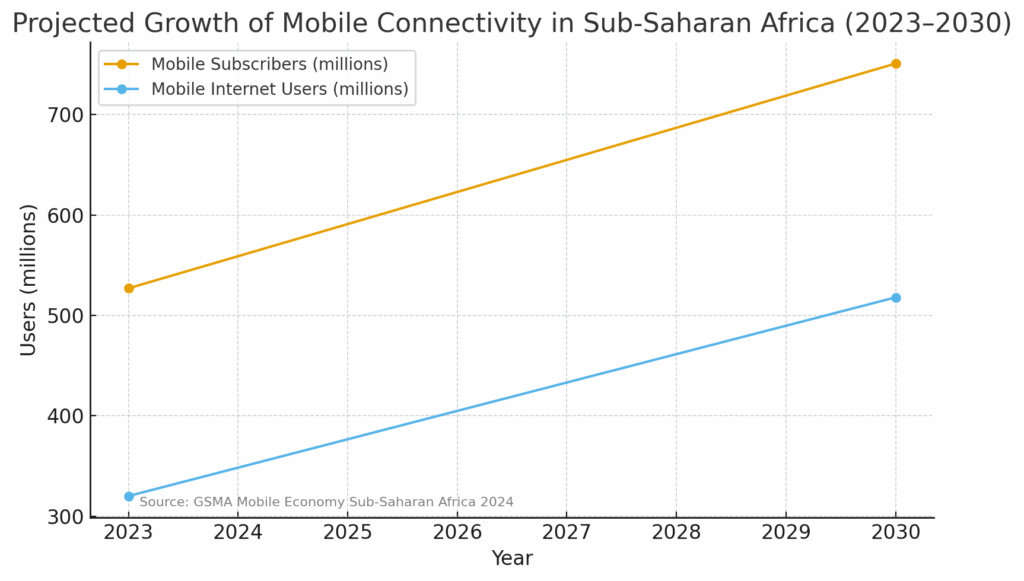

Sub-Saharan Africa (SSA) alone counted 527 million unique mobile subscribers in 2023, a figure forecast to reach 751 million by 2030. Over the same period, SIM connections (excluding licensed cellular IoT) are expected to grow from 1.0 billion to 1.4 billion. Mobile internet users are projected to climb from 320 million to 518 million, as device affordability improves and coverage widens.

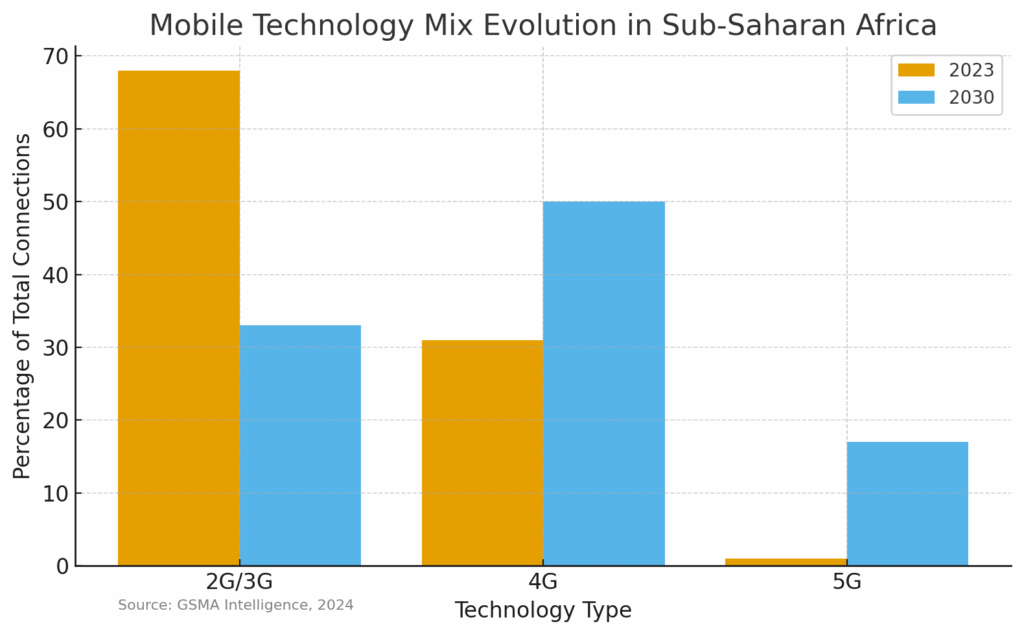

Technology mix is evolving quickly, too. 4G made up 31% of connections in 2023 and is on track to become 50% by 2030. 5G, still nascent in 2023 at 1.2% of connections, is forecast to reach 17% by decade’s end—with fixed-wireless access (FWA) one of the fastest near-term monetization plays for operators. By September 2025, 53 operators in 29 African markets had launched commercial 5G, underlining the step-change from trials to scaled rollouts.

Behind those adoption curves sits a sizable operator economy. In SSA, mobile operators generated $38 billion in revenues in 2023, paid ~$20 billion in taxes across the ecosystem, and the sector supported ~3.7 million jobs directly and indirectly. GSMA estimates 5G alone will add about $10 billion to SSA’s economy in 2030 as vertical use-cases (notably in manufacturing, public administration and ICT) gain traction.

GSMA estimates 5G alone will add about $10 billion to SSA’s economy in 2030 as vertical use-cases

The addressable gap—and why satellites matter

Even with strong momentum, the usage gap is still the world’s widest: ITU’s latest readings put Africa’s internet-use rate at roughly 38%, constrained by affordability, infrastructure deficits and digital-skills barriers. That leaves hundreds of millions of potential users and devices still to connect—an opportunity specially suited to non-terrestrial solutions.

Low Earth Orbit (LEO) constellations and geostationary (GEO) high-throughput capacity are already reshaping the landscape:

- Starlink has expanded at speed since its 2023 African debut, operating in ~19 countries by early 2025 and securing new licenses (e.g., Democratic Republic of Congo in May 2025). After congestion-related pauses in late 2024, it re-opened new subscriptions in several high-demand cities across Kenya, Nigeria, Ghana, Zambia and Zimbabwe in June 2025—evidence of pent-up demand.

- Beyond Starlink, large incumbents and multi-orbit players are busy too: operators across Africa are forming NTN partnerships to extend coverage, offload peak traffic, and add resiliency for enterprises and governments. GSMA’s 2024 SSA outlook calls out “aerial connectivity” (LEO/HAPS) as a rising pillar of universal service strategies.

Quantifying demand, Northern Sky Research (via industry white papers) projects satellite backhaul sites to grow ~60% by 2027, driven by 4G/5G rollout into rural and peri-urban areas where fiber is uneconomic and microwave hops are constrained. This is particularly salient in countries now sunsetting 2G/3G and pushing budget smartphones to accelerate 4G adoption—a move that lifts data demand and, in turn, backhaul requirements.

Capacity, coverage and cost curves are finally aligned with African demand. Backhaul for mobile networks, SME broadband, community Wi-Fi, energy/mining O&G sites, logistics/AGV tracking, and government networks are all scaling end-markets.

What this means for satellite companies: capacity, coverage and cost curves are finally aligned with African demand. Backhaul for mobile networks, SME broadband, community Wi-Fi, energy/mining O&G sites, logistics/AGV tracking, and government networks are all scaling end-markets. Multi-orbit portfolios (GEO+MEO+LEO), software-defined payloads, and open, virtualized ground segments reduce time-to-serve and let providers price to local realities.

The prize for non-African operators: partner, localize, and scale

For telecom groups and satellite providers headquartered outside the continent, Africa is a growth market with partnership DNA:

- 5G FWA and SME fiber-alternatives. In cities with patchy fiber and high right-of-way costs, 5G FWA bundled with managed Wi-Fi is a fast on-ramp to ARPU uplift. Where spectrum and power costs bite, offloading via LEO during peaks can make the unit economics work. GSMA Intelligence highlights FWA as one of the biggest near-term revenue opportunities from 5G investment in Africa.

- Open network APIs and fintech adjacencies. South African operators launched GSMA Open Gateway APIs (Number Verification, SIM Swap) in 2024—an early template for scaling digital identity, fraud prevention and CPaaS across the region via standardized APIs that global developers can consume. Combine that with Africa’s world-leading mobile-money rails, and you have a platform to localize cloud communications, IoT billing and embedded finance at speed.

- Carrier-satellite co-builds and wholesale. Wholesale satellites for universal service (schools/clinics), enterprise VPNs for mining/agri corridors, and resilient back-up for data centers (after 2024’s subsea cable disruptions) are natural joint ventures. Starlink’s fast licensing run has already spurred price competition and partnerships across telcos, a sign that hybrid models (resell, bundle, integrate) will dominate.

Leapfrogging: how Africa can skip legacy and go straight to “latest”

Africa’s connectivity story has always been about leapfrogging—from mobile money to last-mile solar. The next wave will look like this:

- 4G now, 5G where it counts. Operators can prioritize dense urban zones and industrial corridors for 5G (with FWA for homes/SMEs), while using optimized 4G elsewhere. Affordable devices (including sub-$150 5G handsets) and traffic-steering to satellite backhaul where fiber is missing allow near-term performance gains without continent-wide 5G overbuilds.

- Non-terrestrial networks as standard. Instead of treating satellite as a last resort, Africa can embed NTNs into the primary design: mobile backhaul augmentation during festivals, harvest seasons or elections; LEO-first community Wi-Fi for education/health posts; multi-orbit SD-WAN for banks and government. With satellite backhaul sites expected to surge, operators can jump directly to multi-path, software-defined networks tuned for cost and QoS.

- Open RAN and cloud-native cores. Open RAN plus cloud cores reduce vendor lock-in and let African carriers adopt best-of-breed radios, energy-smart RUs, and AI-driven optimization. That matters in power-constrained markets where diesel-heavy sites cut into margins—a challenge GSMA flags as a structural headwind, but also a target for leapfrogging with efficient hardware and smarter orchestration.

- API-first growth. With Open Gateway gaining ground, Africa can skip proprietary integrations and go straight to global, standardized telecom APIs for identity, quality-on-demand, device status, and location. That unlocks developer ecosystems and B2B2X models (logistics, ag-tech, telehealth) much faster than in prior generations.

- Resilience by design. The rise in intentional internet shutdowns and cable incidents has elevated resilience from afterthought to board priority. Multi-homed networks using satellite failover, regional peering, and cached CDNs can keep essential services online—an area where satellite operators can be strategic partners, not just bit-pipes.

Affordable devices (including sub-$150 5G handsets) and traffic-steering to satellite backhaul where fiber is missing allow near-term performance gains without continent-wide 5G overbuilds.

What success looks like—for Africa and for global players

For policymakers, the priorities are clear: affordability (tax reforms on devices/services), spectrum roadmaps aligned to WRC-23, and effective universal service funds that crowd-in private capital rather than distort it. The payoff is tangible: more citizens online, stronger digital public infrastructure, and a bigger tax base from a healthier telecom economy.

For operators and satellite companies based outside Africa, winning strategies share a few traits:

- Local partners first. Team with MNOs/ISPs on FWA, community Wi-Fi and enterprise bundles; use wholesale where licensing takes time.

- Design for power, price and logistics. Offer ruggedized CPE, solar-friendly sites, usage-based pricing, and remote-ops toolchains (zero-touch install, remote beam switching).

- Build enterprise verticals. Mining, energy, agriculture, logistics and government are ready for managed connectivity, edge computing and data-gravity solutions that ride on hybrid terrestrial–satellite backbones.

- Prove the economics. Pilot with quick-win clusters (industrial parks, special economic zones, tourist corridors), show TCO vs. fiber/microwave, then scale.

Africa’s telecom and satellite markets are not just “emerging”; they are re-shaping how networks will be built globally—open, hybrid, resilient, and financially inclusive. For international operators and satcom providers willing to localize offers and share risk with regional partners, the upside is large, immediate, and sustainable. The continent’s next leap is underway; the smart money is moving with it.